2012 Annual Report

Home Page

Introduction

Management and Corporate Governance Practices

Financial Information and Risk Management

Türkçe

An Assessment of 2012: Strategies, Developments and Targets for the Future

During 2012, Ziraat Bank uninterruptedly carried on with its efforts towards the "Bank and Ziraat Customer" structuring.

During 2012, Ziraat Bank uninterruptedly carried on with its efforts towards the “Bank and Ziraat Customer” structuring formulated with a view to fulfilling the financial needs of its customers through the right channel, at the right time, and with the right value propositions.

Through this change and transformation project, the Bank intends to achieve increased efficiency and productivity in its customer relationships, and lending processes and policies.

Having successfully completed yet another operating period, Ziraat Bank set its financial management strategy as:

In 2012, Ziraat Bank captured marked upward trends in profitability and productivity ratios.

Balance sheet size aligned with shareholders’ equity

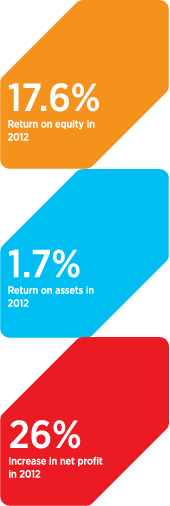

Molding its activities so as to attain a well-balanced balance sheet structure, Ziraat Bank’s total assets were worth TL 162,868 million as at year-end 2012. Aiming to render profitability sustainable, which is an important component of shareholders’ equity, the Bank posted year-end net profits in the amount of TL 2,650 million, up 26% year-to-year.

In parallel with the increased profit, the Bank captured marked upward trends in profitability and productivity ratios, which also take place among the Bank’s important agenda items. 16.1% in 2011, return on equity (RoE) went up to 17.6% in 2012. Similarly, return on assets (RoA) also increased and rose from 1.3% in 2011 to 1.7% in 2012.

Worth TL 71 billion at year-end 2012, Ziraat Bank’s total lending took 44% share of the Bank’s balance sheet.

As at 2012, the Bank’s total deposits amounted to TL 119 billion, and the share of deposits to total liabilities was 73%. Savings deposits made up the greatest portion of deposits with 48%.

Continuously expanding domestic service network

Turkey’s most extensive bank, Ziraat Bank carried on with its efforts to expand its service network at full speed also in 2012. The total number of the Bank’s domestic branches reached 1,425 including the newly created 5 corporate, 27 commercial and 77 entrepreneurial branches, and continued to serve solo to fulfill the people’s banking needs at 404 locations in Turkey.

As at year-end, Ziraat Bank’s service network consisted of 1,490 domestic points of service made up of;

Within the scope of domestic branch network expansion efforts, Ziraat Bank will keep opening new branches in the future, with a particular focus on İstanbul and districts where no other bank is present, and continue to contribute to the country’s employment.

New business model structuring under the change and transformation project

Under the change and transformation project in progress, Ziraat Bank is formulating a new business model that will be able to respond more effectively to its customers’ needs. The new business model redefined the Bank’s code of conduct, carried out customer segmentation, redesigned regions and branches in alignment with this segmentation, and created a matrix organizational structure with domestic and overseas subsidiaries.

Within the scope of the Bank’s new organizational structure, the customers were categorized as follows according to their financial needs:

Along this line, branches were diversified as Entrepreneurial Branches, Corporate Branches, Commercial Branches and Branches depending on the type of customers they serviced, so as to ensure customized service delivery.

More than 40,000 new customers have been acquired for the Bank under the entrepreneurial segment.

Entrepreneurial Banking

In 2012 during which Ziraat Bank was in the process of change and transformation, the Bank worked heavily to switch to the Bank Customer Service Model, which was molded on the “Customer-Oriented Banking” concept.

In this context, customer and branch segmentation were brought to completion and portfolio management was launched to ensure that the right services are delivered to the customers effectively through the right channels.

Customers are offered service efficiently by 241 Customer Relationship Managers (CRMs) and 212 Customer Relationship Assistants (CRAs) at the 77 Entrepreneurial branches opened during 2012, and by 1,138 CRMs and 800 CRAs at 748 branches operating under the Bank Customer Service Model, for a total of 1,379 Entrepreneurial CRMs and 1,012 Entrepreneurial CRAs.

Below is a summary of the activities carried out within the scope of entrepreneurial banking in 2012, when a switch was made to the Bank Customer Service Model:

Ziraat Bank developed synergetic cooperation with numerous national and international agencies to provide long-term financing to the SMEs that account for a substantial portion of commercial and economic activity in our country, to contribute to their operating capitals, and to support their growth.

World Bank loans for small and medium-sized enterprises

The World Bank’s loans are set apart from the other loans available in the sector in that they provide long-term, low-cost investment and operating finance with grace periods and flexible repayment terms. Ziraat Bank continued to channel the loans secured from the World Bank to the SMEs in 2012, which had been started to be allocated in 2010.

Within the scope of the Access to Finance for SMEs Project, businesses’ access to financing were given increased depth and breadth with the modified legislation during 2012, in line with the understanding to offer the funds secured from the World Bank for fulfilling the financing needs of small and medium-sized enterprises with the right value proposition.

The contacts for obtaining medium- and long-term funds from the World Bank continued throughout 2012, and a new collaboration is planned to be put into life within the framework of a new project in 2013.

EIB loan for the operating capital needs of SMEs

In 2012, Ziraat Bank arranged a loan in the amount of EUR 100 million from the European Investment Bank (EIB) for which the guarantor was the Turkish Treasury. The loans extended in this frame are intended to fund the investments the SMEs will make in Turkey and their operating capital needs in an effort to support the growth of SMEs through increasing their production, productivity and employment.

Planning to renew the project in 2013 that achieved a high success level of realization, Ziraat Bank will continue to provide financing support to its SME customers through the additional resource to be obtained.

“My First Business, My First Bank” loan collateralized by the European Investment Fund

A guarantee agreement incorporating collateral for the cash loan volume of TL 300 million has been signed by and between the European Investment Fund (EIF) and the Bank for financing the operations of the SMEs at inexpensive costs without imposing the burden of additional collateral for their access to funds.

Under the agreement, the EIB-Collateralized “My First Business, My First Bank” SME Loan that will be allocated from the Bank’s resources is intended to back newly-established SMEs and tradesmen and particularly women entrepreneurs that are in need of collateral and start-up capital. In addition, Ziraat Bank practices positive discrimination for women entrepreneurs by offering them additional interest rate discounts, longer terms, and grace period options.

Within the scope of the collateral support program secured from the EIF by year-end 2011, the Bank started allocating loans in the amount of TL 50,000 in 2012 to small entrepreneurs who will start up a new business or who own businesses younger than 5 years against their personal guarantee. Significantly helping the businesses that recently start operations with their access to external funds, the project is intended to lend support to Turkey’s young and dynamic entrepreneur force.

Incentive for the development of export companies

In 2012, Ziraat Bank cooperated also with resident financial institutions to support the SMEs. The representative of the Turkish private sector, Foreign Economic Relations Board (in Turkish: DEİK) launched a project that will increase the exports of the Turkish machinery industry with the support to sharpen competitiveness and formulate export strategies, which will enable the achievement of the Ministry of Economy’s target to reach USD 500 billion in exports by 2023. For the project, the Bank executed a protocol with the DEİK.

Under the protocol, companies applying to the Bank are offered 75% subsidy for utilizing the services of needs analyses, training and consultancy, overseas marketing (joint market research, market visits, trade delegations, visits to overseas trade shows, matching and group introduction activities), purchasing delegations and personal consultancy via the contractor firm.

Acting as the solution partner of export companies through its overseas service network, Ziraat Bank provided an incentive of up to USD 200,000 for the preparation of strategy reports, again in cooperation with the DEİK. These reports will help businesses penetrate international markets and serve to their integration with the global economy.

Support to the domestic machinery manufacturing industry

Ziraat Bank is the greatest supporter of the companies engaged in the manufacturing and exportation of domestic machinery, as well as companies that need financing for the purchase of domestic machinery.

Intended for fulfilling these companies’ investment needs for purchasing new domestic machinery from Turkey, their operating capital requirements that result from the investment, and their foreign trade financing needs, preparations for the loan package were completed during 2012 and it will be put in use for entrepreneurial customers during 2013.

Within its primary targets, Ziraat Bank attaches top priority to the development and growth of the agricultural sector and its acquiring global competitive strength.

Efficient cooperation with KOSGEB and Türk Eximbank

Ziraat Bank efficiently cooperates with KOSGEB (Small and Medium Enterprises Development Organization) and Türk Eximbank to allow customers to quickly benefit from non-Bank-funded export loans besides offering attractive Bank-funded FX loan facilities to the exporters.

Offering inexpensive TL/FC operating loans to exporter companies, the Bank also makes available the forwards instrument with special advantages, which protects the businesses against volatilities in exchange rates. An important business partner of Türk Eximbank, the Bank intermediates the allocation of pre-shipment export loans and SME pre-export facilities. The Bank also carries out letter of credit and acceptance/endorsement transactions and prefinancing transactions for import trade financing.

Standing by and supporting the SMEs also through the rough times, Ziraat Bank postponed the debts of SMEs that have sustained losses in the Van Earthquake of 2011. In addition, the Bank joined the KOSGEB’s interest support program launched for the SMEs by reason of the earthquake, and thus, continued to extend support to the SMEs.

Sector-specific support packages

The Pharmacist Package was introduced in 2012, which was aimed at satisfying the operating capital, medical equipment financing, and place of business and vehicle purchases of the Bank’s customers active in the pharmaceuticals industry.

In addition, the Tourism Support Package was offered for the short-, medium- and long-term operating finance needs of the tourism sector and its interacting sectors, as well as for their borrowing needs that can be considered within the context of “new investment” and “renovation loans”. The package incorporates flexible repayment alternatives that suit the relevant sector, grace period options, and advantageous interest choices.

By the side of the customer in agricultural banking

Within its primary targets, Ziraat Bank attaches top priority to the development and growth of the agricultural sector and its acquiring global competitive strength.

Taking place in every phase of financing the agricultural production, agricultural industry and industrial production on the back of the transformation it launched in 2012, the Bank took into consideration the resulting added value, and set it as its main target to work with all actors along the value chain.

In agricultural industry, Ziraat Bank stands by its customers in all phases of production from the soil to the shelf, from the production of products to their sales and marketing in and out of the country, in brief through all processes of the economy from the first product to its delivery to the end consumer.

TL 20.7 billion loan for financing the agricultural sector

At the end of 2012, Ziraat Bank’s lending for financing the agricultural sector amounted to TL 20.7 billion and the number of its credit customers reached 602,167.

Within these loans, the year-end balance of the loans extended from the Bank’s resources amounted to TL 17.9 billion, which was extended to 500,789 credit customers, while the balance in loans arranged from funds was worth TL 2.8 billion, which was made available to 101,378 customers.

During 2012, 262,591 real person or legal entity customers were extended loans worth TL 6.7 billion from the Bank’s resources, and 32,186 producers received loans worth TL 515.1 million from fund resources.

48% of Ziraat Bank’s agricultural loan book is made up of medium-long term investment loans with a balance of TL 8,577 million, and 52% of short-term operating loans worth TL 9,319 million.

Interest-free stockbreeding loans

In August 2010, Ziraat Bank launched the Interest-Free Stockbreeding Loans to meet the modernization and capacity increase needs of existing cattle and small cattle husbandry and breeding enterprises, and to support new stockbreeding enterprises. Under the program, the loans extended to 9,755 producers amounted to TL 455 million in 2012. Interest-Free Stockbreeding Loans yielded a balance of TL 4,341 million and the number of producers stood at 68,193 as at year-end 2012.

Ease of financing for 380,000 producers with Başakkart

380,000 producers using the TL 1.3 billion portion of the agricultural credit line of TL 1.9 billion with Başakkart in 2012 purchased agricultural inputs and services including fuel oil, seeds, fertilizers, pesticides, feeds and veterinary services from 12,428 member merchants with interest-free repayment terms of up to five months, and thus eased the financial burden on their production processes.

Fixed-interest tractor loans

Under the Fixed-Interest Tractor Loan Product, the Bank extended TL 602 million in loans to 18,847 producers in 2012. Within the scope of this implementation conducted since 2004, the loans made available to a total of 108,804 producers amounted to TL 3,241 million.

Single-digit interest rate on agricultural loans

In 2012, Ziraat Bank applied 10% interest rate on operating loans with a term of one year or shorter from within Bank-funded agricultural loans, and 12% on those with a term of longer than one year. Producers had the possibility to obtain agricultural operating and investment loans with annual interest rates varying from 0% to 9% within subsidy ratios set on the basis of production scopes in relevant decrees. Within this frame, the loans extended to 239,345 customers amounted to TL 5.6 billion in 2012; overall, total loans supplied to 4.4 million producers in the past 9 years were worth TL 48.2 billion.

Contribution to the integration of agriculture and industry

In 2012, protocols were signed with 17 companies operating in the seed, sugar beet, trout and poultry industries, and approximately 16,000 contracted producers of these companies were provided the opportunity to get operating and investment loans with suitable conditions and with a total line of TL 158 million.

Mediation services

During 2012, Ziraat Bank mediated in the payment of:

Greenhouse cultivation loans

Under this heading, Ziraat Bank extended TL 219 million in loans to 4,951 producers. The loans supplied to a total of 78,232 producers in the last 9 years for financing greenhouse construction, modernization, cultivation activities and similar needs amounted to TL 1.8 billion.

In 2012, corporate and commercial segment cash loans expanded by 36.6%, whereas non-cash loans were up by 33.9%.

Corporate and Commercial Banking

Ziraat Bank targets to make sure that its corporate and commercial banking products and services are competitive in the sector and satisfy the customers’ needs, and creates costless resource and cross-sales opportunities with related activities.

Customer-oriented approach to banking

The change and transformation activities conducted by Ziraat Bank in 2012, and the relevant training offered to employees were intended to integrate customer-oriented sales, high productivity, healthy growth and sustainable profitability into the Bank’s code of conduct, as well as to create a new understanding of working across the Bank.

As part of these efforts, the Bank estimates that the number of its active customers will increase on the back of a productive customer management that will be implemented via 5 Corporate and 27 Commercial Branches that went into service in 2012.

During 2012, the Bank added momentum to customer and branch segmentation within the frame of customer-oriented approach to banking, defined the rules of segmentation, made the necessary revisions to the corporate and commercial lending system infrastructure, and assigned the Bank’s customers to relevant segments.

With the portfolio management screens installed, customer view screens made widespread, product infrastructure revised, and the pricing infrastructure indexed to LIBOR/EURIBOR/TRLIBOR, the work on the bank’s system infrastructure was brought to completion.

February 2013 will see the introduction of the software for portfolio management, for which the necessary work is ongoing, and for the FTF-based (Fund Transfer Pricing) interest structure and interest commission pricing infrastructure required by the new structuring.

In 2012, corporate and commercial segment cash loans expanded by 36.6% and reached TL 10.7 billion, whereas non-cash loans were up by 33.9% to TL 13.4 billion.

In 2013, Ziraat Bank will continue and further increase its efforts focused on the financing of the real sector and broadening its commercial customer portfolio. The Bank regards the year ahead also as a year of greater emphasis placed on marketing activities addressing commercial companies that remains outside the corporate scale.

Ziraat Bank’s priority target and strategy for the coming year include increasing the share of corporate and commercial lending portfolio to the Bank’s balance sheet, constantly enhancing the quality of service and ensuring customer loyalty through building long-term, versatile relationships with customers.

High quality service and modern products in cash management

Ziraat Bank painstakingly fulfills its role in the sector as a market maker with its rational pricing and competition strategy. The Bank espouses a pricing strategy that is not aggressive, places emphasis on broad-based deposits, and develops policies seeking to promote saving tendency and to attract small savings to the Bank.

Carrying on with its customer-oriented, effective and productive cash management practices at full speed during 2012, Ziraat Bank increased the number of institutions/companies under protocol for collection/payment/general banking/direct debit system to 527.

During the reporting period, the collections performed for 71.3 million transactions using the Corporate Collection Systems were worth TL 81.5 billion, from which TL 883 million was derived as average demand deposits. On the other hand, 14 million transactions were referred to non-branch channels, reaching 50% non-teller ratio as a result of the actions taken to alleviate the heavy transaction burden on branches.

Ziraat Bank will keep building on its relationships with its corporate and commercial customers in the coming years by offering high quality service and modern products within the scope of cash management modules.

Retail Banking

Ongoing transformation in Retail Banking

On the back of the change and transformation program initiated in December 2011, Ziraat Bank set it as its main strategy to be an innovative and pioneering bank that better analyzes customers’ needs, that stands closer to its customers and that creates more value.

In this framework, in 2012 the Bank reengineered its service model also in retail banking, which is the main building block of change and transformation, on the aspects of customer, product, channel, organization, process and technology, human resources and location.

Structuring efforts have been carried out on many different axes:

One of the crucial steps of the operational transformation in retail banking was the revised credit management and performance management process in 2012.

In this framework, lending processes have been revised and credit and financial analysis systems have been developed that will provide more efficient and more dynamic measurement of the credit risk, including centralized allocation.

On another hand, the performance management system has also been remade on the basis of the “balanced scorecard” approach in unit and individual level to ensure that the strategies defined within the frame of the change and transformation program are successfully implemented. As of year-end 2012, the system’s integration has been finalized, and the new performance system was put into practice in all branches that have completed their transformation from the start of 2013.

Within the scope of bancassurance activities, Ziraat Bank maintained its leadership particularly in the life insurance sector in 2012.

Leadership in the retail segment

Preserving its position as the sector’s leader in the number of retail customers, Ziraat Bank offered uninterrupted service all over Turkey to its more than 25 million customers via its 1,425 retail branches and over 23,000 employees during 2012, which also saw intensive competition.

In the retail segment that has 45% share within Ziraat Bank’s total loan book, the credits supplied to retail customers amounted to TL 29 billion. Remaining the sector’s leader by a large margin with TL 19 billion in consumer loans extended to over 2 million customers during 2012, Ziraat Bank registered 32% growth in “Salary Advance” and “Deposit Advance” products, which are the firsts of their kinds in the sector and which are intended to fulfill the short-term needs of customers.

In another department, the Bank made available TL 3.3 billion in loans to 200,000 customers in as short a period of time as 3 months with the “Four Seasons Loan Package” designed to cater to all of the basic banking needs of retail customers in 2012.

Commanding 69% share of Ziraat Bank’s total deposits, retail banking achieved a magnitude of TL 73 billion during 2012, in line with its strategy of new product development aligned with customer needs and broad-based deposits. Core deposits have approximately 70% share of total savings deposits.

In 2012, Ziraat Bank introduced the “Grateful Account” which encourages customers who entrust their savings to Ziraat Bank for a prolonged period of time and rewards them with higher returns. The implementation was quickly embraced by the customers and reached a high volume.

Ziraat Bank launched “Gold Term Deposit Account” for those customers who tend to save up in gold coins and wish to benefit from the advantages of term deposits along with the value increases in gold for gram equivalent of gold coins of 1000/1000 purity (A02), and gold term deposit accounts accumulate interest with flexible maturity options.

In an effort to rechannel the gold coins traditionally “kept under the pillows” back into the economic cycle, “Gold Time” initiative was introduced in 2012, under which physical gold coins were received by the contracted firm thus allowing them to be deposited in the customers’ gold term deposits with the Bank.

Within the scope of bancassurance activities, Ziraat Bank maintained its leadership particularly in the life insurance sector in 2012, and its total premium production topped TL 1 billion including the premium volume in the non-life branches that grows with the special advantages provided to customer groups.

New methods in lending processes

In order to offer faster, higher quality and more satisfactory service to its retail loan customers that make up a large portion of its loan book, Ziraat Bank reviewed its lending processes and introduced a number of new methods.

Within the frame of efforts to centrally evaluate retail loan demands by way of scoring method, the Centralized Allocation went live in May 2012 for the following purposes:

Allocation decisions are started to be made by the Decision Module and the Head Office Allocation Center.

The calculations based on the transaction handling times revealed that centralized transactions provide much higher efficiency as compared to those handled by branches. As of year-end 2012, almost all of the branches switched to the centralized allocation structure. It is planned to incorporate the few number of remaining branches in the system during 2013.

In 2012, Ziraat Bank extended a total of 1,359,852 retail loans, which were worth TL 12.3 billion.

For the purpose of linking the retail loans of customers to a new repayment plan that suits their income and cash flows and/or ensuring smooth recovery through granting an extension of maturity, a total of 782 retail loan products amounting to TL 15.7 million were restructured during 2012, and 685 customers benefited from restructuring.

Efficient electronic service channels

Ziraat Bank delivers efficient and quality service to its retail customers through electronic service channels, as well as its countrywide branch network.

Debit cards

• 15% increase in the number of Bankkart

The sector’s leader in debit cards, Ziraat Bank grew the number of its Bankkart (Ziraat debit cards) cards by 15%. The number of Bankkart cards increased by 2,481,494 compared to the end of 2011 and reached 18,994,470, while the number of TSK (Turkish Armed Forces) chip debit cards rose to 612,359. The Bank derived a turnover of TL 69.7 billion on its Bankkart cards, which was up by 34.7% as compared to its year-end 2011 value of TL 51.7 billion.

• 30% expansion in credit card turnover

While the number of credit cards issued by Ziraat Bank reached 3,423,816 in 2012, its turnover on credit cards was up by 30% and reached TL 10 billion. The ratio of active cards went up from 45% to 48%.

• Number of POS devices draw near 130 thousand

In 2012, the number of POS devices provided by Ziraat Bank increased by 13% and reached 126,905. The turnover of member merchants, on the other hand, grew by 27% to reach TL 7.6 billion.

During 2012, the Bank collected TL 535.7 million in social insurance (SGK) premium payments on behalf of the Institution, which can be collected by the Bank’s virtual POS from any credit card.

• Card-based solutions in public transport

Under the transportation projects co-conducted by Ziraat Bank and the Interbank Card Center (in Turkish: BKM), the infrastructure work has been completed for the use of the Bank’s banking cards in public transport vehicles operated by Konya Metropolitan Municipality and Tarsus Municipality.

• Cooperation with TURSAB

The Bank supplied the POS devices for the museum kiosk implementation realized in cooperation with the Ministry of Culture and the Association of Turkish Travel Agencies (in Turkish: TURSAB), and devices were installed at the Topkapı Palace and Ephesus ruins in İzmir. The work is underway for installing the devices at the Sultanahmet Square, Hagia Sophia, Archaeological Museum (İstanbul), and Tourism Information (İstanbul).

Development work has been finalized that will enable transacting in foreign currency (EUR and USD) with foreign credit cards on the Bank’s POS devices, which have been successfully spread across all branches in 2012. In order to increase the productivity and profitability of the project, the GBP, JPY and RUB currencies will also be integrated into the system during 2013.

Alternative delivery channels

The number of Internet banking customers reached 1.8 million.

The number of Ziraat Bank’s registered internet banking customers grew a remarkable 61% and went up to 1.8 million by the end of the year. In parallel, financial transactions performed on the internet branch was up by 54% from 20 million at year-end 2011 to 30.9 million at the end of 2012, while the volume of financial transactions which was worth TL 60 billion boosted by an amazing 361% to reach TL 277.7 billion.

The Bank’s corporate internet site was revamped in design and technology, and constructed in a manner that allows active marketing of all products, campaigns and novelties, making life easier for customers, and working compatibly with smart devices (phones and tablets).

The key new features of the website included the tool that enables non-internet banking customers to make online application for the internet branch, easy access with the option to set PIN on the website for those who cannot recall their internet banking entrance PIN, and loan/deposit/investment/card calculation and application modules.

At the end of 2012, the number of the Bank's active ATMs rose by 11% year-on-year to 4,231.

11% increase in the number of ATMs

At the end of 2012, the number of the Bank’s active ATMs rose by 11% year-on-year to 4,231, while the number of its ATMs offering the cash deposit feature reached 1,425. With their installation started in June 2012, 95% of 1,500 new generation ATMs was completed by the end of the year. Furthermore, 1,000 ATMs with cash deposit feature were purchased and plans were prepared for their locations.

ATMs with cash deposit feature also enable making the payments for the Ministry of National Education exams, Measurement Selection and Placement Center (ÖSYM) exam fees, Motor Vehicle Tax payments (from the account), centralized payment with palm, EFT, bill payment with credit card, SGK payment, dormitory rent payments, Loans and Dormitories Administration (KYK) fee payments, title deed charge payments, and cardless Motor Vehicle Tax payments. Also, ATM menu developments were finalized.

The ratio of ADC use rose from 60.1% in 2011 to 94% at the end of 2012 for bill collections, and from 6.5% to 31.8% for non-bill collections during the same period of time.

Treasury and Strategy Management

In essence, the Treasury and Strategy Management Group manages the risks carried on the balance sheet; determines interest rate, exchange rate and liquidity scenarios; implements the policies determined; revises the policies in line with the changing internal and external conditions, and offers centralized pricing service for treasury and investment instruments to all branches.

The objectives of the Treasury and Strategy Management are spelled out as follows:

In addition, the objectives of the Treasury and Strategy Management Group have been expanded to include the creation, development and management of the central treasury function of the overseas branches, banks and domestic subsidiaries, within the frame of the Ziraat Finance Group that is in the process of development.

Besides liquidity management and investments in borrowing instruments similar to eurobonds/bonds in view of the risk/return balance of the Bank’s balance sheet, the Bank took place among the active players in the money, foreign currency and capital markets for fulfilling the customers’ needs in contact with the marketing and sales groups within the frame of customer-oriented approach to banking in 2012.

In the reporting period, efforts continued to more effectively manage the Bank’s assets/liabilities and the financial risks involved in the balance sheet. The Bank’s customers were offered alternative banking products, and investment and funding facilities were diversified within the frame of the asset/liability management strategies that are being pursued.

As one of the market maker banks in the Turkish bonds and bills market as determined by the Undersecretariat of the Treasury of the Republic of Turkey, Ziraat Bank successfully maintained its market maker position in 2012. As one of the active participants in the primary and secondary bonds and bills markets, the Bank’s profit generated on capital market transactions shows a rising trend.

Increased diversity in treasury products

The creation of the centralized treasury function contributed to increasing the product diversity through new treasury products within the scope of the development of the “Ziraat Customer” and ultimately “Ziraat Finance Group Customer” concepts in the Ziraat Bank’s ongoing change and transformation process. Along this line, customer transaction volumes in treasury products were increased through competitive pricing and effective customer relationship management, by making use of the extensive branch network and the constantly improved alternative delivery channels.

In order to effectively meet the needs of customers with different risk/return profiles, the Bank issued two Type B 100% Capital Guaranteed Sub-Funds under the Capital Guarantee Umbrella Fund during 2012. Having defined its mutual funds management strategy as issuing thematic and capital guaranteed funds for the most part, Ziraat Bank will continue with fund issues in 2013.

To increase the diversity of funding and enhance its quality, and to support the extension of average funding term, bank bonds/bills in Turkish lira issues started in February 2012, and five issues amounted to TL 4 billion in public offerings.

As at December 2012, the BRSA’s permission has been received for a total issue of TL 7 billion. Within this scope, the Bank will continue with issues of different maturities in 2013.

Using structured financial products, not only the risks in the Bank’s balance sheet were managed, but also alternative investment and funding resources were developed. The Bank will continue to diversify the funding structure with non-deposit financing resources such as eurobond issues and syndication loans in 2013 and thereafter.

Swift and high quality foreign trade transactions

Enjoying the capability to reach any point in the world from any point in Turkey thanks to its extensive domestic branch network and the overseas service network made up of branches, subsidiaries and correspondent banks, Ziraat Bank conducts international banking transactions swiftly and at a high quality both domestically and globally.

Foreign trade transactions at Ziraat Bank are started to be carried out from 5 Corporate Branches and 27 Commercial Branches across the country, in addition to the units located in İstanbul and Ankara so as to provide faster and more effective solutions to the customers’ needs. Financing needs of foreign trade customers are responded to in a fast and effective manner at appropriate terms and prices, in conjunction with the financial institutions abroad.

The Bank’s foreign trade transactions are carried out by competent personnel who hold Certified Documentary Credit Specialist (CDCS) Certification (26 certificates) and Certificate in International Trade and Finance (CITF) (8 certificates).

At Ziraat Bank, foreign transactions are conducted via 50 nostro accounts with the Bank’s overseas correspondent banks and 79 vostro accounts at the Bank of other domestic/overseas banks and overseas branches and subsidiaries.

The foreign currency transfers by and between the seven resident banks that belong to the DTR (FX Transfer) system, which was designed by Ziraat Bank for use in the domestic FX transfers, are carried out quickly and at low costs, without requiring the mediation of overseas banks and directly from such banks’ accounts opened with Ziraat Bank.

Transfers up to a certain limit made to overseas branches and subsidiaries that have vostro accounts with the Bank and to domestic banks included in the DTR system are directly carried out by the branches without any further interference, and thereby assure low-cost and maximum speed in transactions.

The Bank’s customers can withdraw money from their accounts in domestic branches or the branches in the TRNC online via Ziraat Bank branches abroad or subsidiary banks. It is planned to soon complete the work, which will enable them to deposit money into their accounts in Turkey using the same channel.

Solid and deep-rooted international relations

The solid and extensive international service network built on solid foundations all over the world makes up an important part of the concept “Ziraat Finance Group” developed by Ziraat Bank within the scope of its change and transformation strategy.

The Bank pursues its activities with the goal of maintaining its efficient and respected position enjoyed in the international banking arena, and offering banking products and services that will win value for its customers, with a particular emphasis on financing the foreign trade between Turkey and the geographies where it operates via its overseas branches and subsidiaries.

At the end of 2012, Ziraat Bank maintained its strong and deep-rooted correspondence relations with approximately 1,300 banks in 119 countries. The Bank’s broad correspondent network is continuously improved and updated in parallel with customer needs, as well as the conjuncture and trends in the world economy.

The Bank works in close cooperation with export insurance agencies and country Eximbanks throughout the world. The Bank signs framework agreements with various correspondent banks in order to mediate the loans to be provided by these agencies to its customers.

Having mediated in successful transactions aimed at diversifying funding resources and providing longer-term and low-cost financing to its customers in 2012, the Bank keeps working towards the target of sharpening its competitive edge.

With branches, representative office and subsidiary banks at 75 locations in 16 countries, Ziraat Bank maintains its position as the bank with the largest international service network of any Turkish bank.

Global service network

With branches, representative office and subsidiary banks at 75 locations in 16 countries, Ziraat Bank maintains and further strengthens its position as the bank with the largest international service network of any Turkish bank. The Bank’s global points of service continue to work actively with the mission of delivering higher quality service by way of launching new products and projects in the countries where they are present. Their locations are presented below:

Efficiency and expansion projects

Ziraat Bank continues with its operations with the target of becoming Turkey’s and the region’s strongest and most efficient bank in the period ahead, by capitalizing on potential opportunities at every location where it has a presence based on the analysis of developments in global markets. To this end, the Bank constantly makes examinations and assessments in line with its target of offering service and expanding its activities at every location that offers development potential and opportunities with respect to business volume and commercial relationships with a special focus on the near geography based on forward-looking projections.

In Bulgaria, Ziraat Bank serves its customers through 4 branches: a central branch in Sofia, and sub-branches in Plovdiv, Kardzhali and Varna. The initiatives in branchless banking are ongoing; it is planned to further expand the scope of operations by soon introducing credit cards, telephone banking and POS products in addition to the debit cards, ATMs and internet banking that have already been launched.

In Greece, Ziraat Bank serves its customers through four branches in Athens, Komotini, Xanthi and Rhodes.

Having begun to offer services in the TRNC in 1974, Ziraat Bank increased the number of its branches in the TRNC to 10, with the opening of 5 new points of service in the Near East University, Gönyeli, Çatalköy, Karaoğlanoğlu and İskele in the last two years. In parallel with its steady expansion trend in recent years, the Bank worked intensively to expand its product portfolio and improve service quality.

Started to be extended during 2011, agricultural loans were received with great interest and reached a volume of TL 40 million by the end of 2012. Total lending, on the other hand, amounted to TL 311 million. Offering all of the banking services available in mainland Turkey, the Bank’s branches in TRNC takes place in the top ranks among all banks operating in the TRNC in terms of size and profitability, and contribute significantly to the national TRNC economy.

Pursuing operations in Georgia since 2001, evaluations are in progress to organize the Tbilisi Branch as a foreign banking subsidiary and to open a sub-branch in Batumi. The Batumi branch is targeted to become operational in the first quarter of 2013.

With the ATM and debit card services launched in Tbilisi, the internet banking service is also planned to be introduced during 2013.

In Saudi Arabia, the Jeddah Branch began activities on 14 March 2011. The branch has added momentum to its efforts to meet the needs of Turkish contracting companies for letters of guarantee, as well as to cover the banking needs of businessmen working in Saudi Arabia and Turkish citizens who visit Saudi Arabia for pilgrimage. At the end of the year, the non-cash lending volume of the branch reached USD 97 million.

Having started service delivery under extraordinary circumstances in Baghdad in Iraq in 2008, Ziraat Bank has become the first Turkish bank to open a branch in Erbil on 14 February 2011. Having continued to mediate in the letters of guarantee requested by Turkish contracting companies operating in the region and in the money transfers of Turkish firms and workers at an increasing rate in 2012, the Erbil Branch attained a non-cash loan volume of USD 114 million at the end of the year.

Human Resources and Training

The elite team possessing superior competencies that have been supporting Ziraat Bank ever since its inception also represents the foundation of customer satisfaction, which is given utmost importance.

Contemporary human resource management system

Having formulated a contemporary human resource management system based on the principles of transparency, participation, efficiency and compliance with banking ethics, Ziraat Bank continually invests in its employees who are the architects of its corporate success.

Recognizing that sustainable success and continual customer satisfaction compel high-performing employees, Ziraat Bank aims to maximize the motivation, knowledge and skill levels of its employees. To this end, all employees are offered systematic training opportunities focused on career and development.

Personal and professional development training programs have been conducted for the entire Bank personnel throughout the year in order to ensure that the Bank Customer Service Model is espoused by the personnel, to standardize the service quality at all points of service, and to build on the employees’ customer relationship competencies.

During 2012, the bank continued to provide the compulsory training programs, which are required to be given within the scope of licensing and laws, as well as the training sessions for personnel that will be newly recruited, and training programs were differentiated according to target groups.