Value to Our Business

I

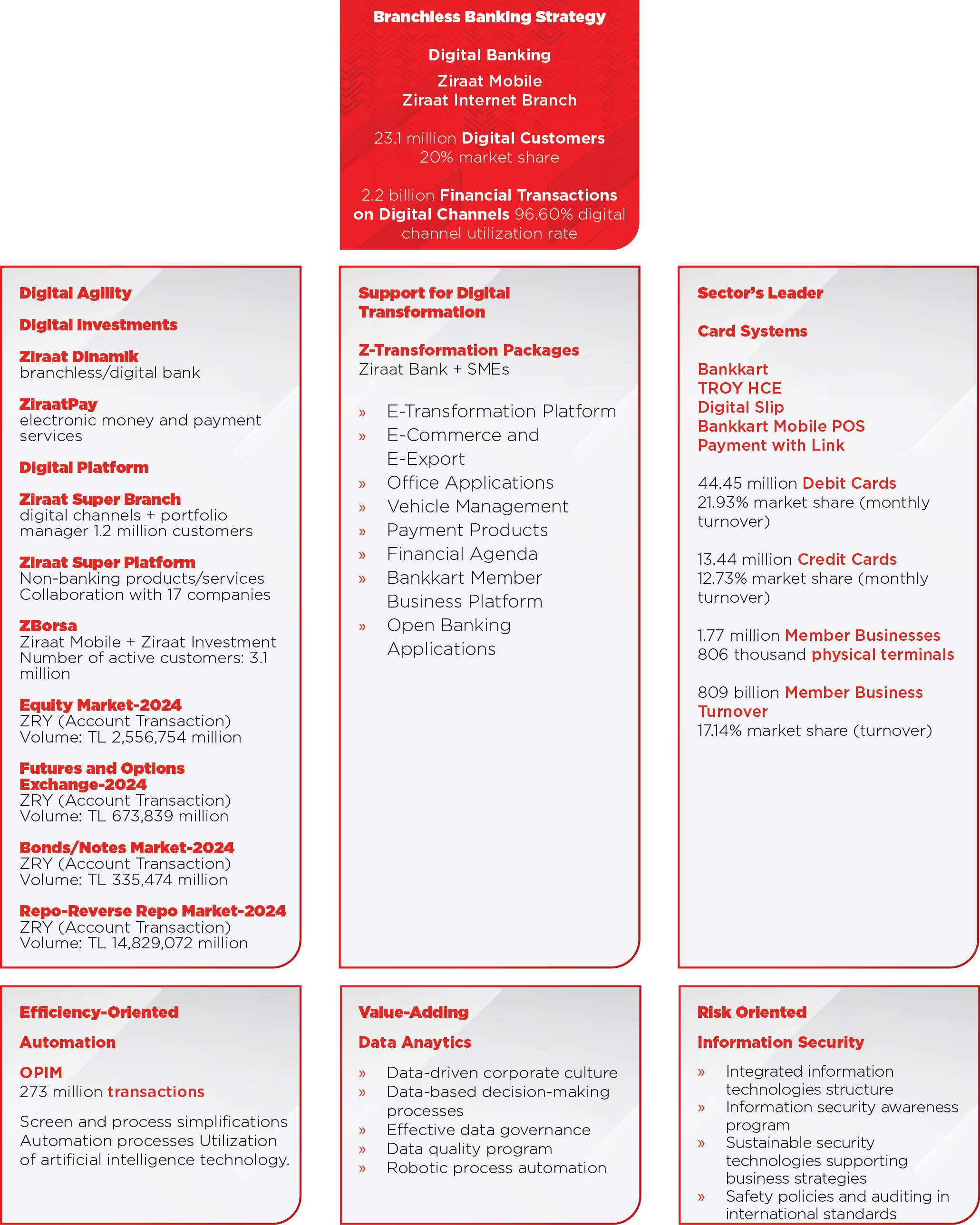

Digital Banking

Total Number of Active Digital Customers

23.1 Million

Number of Financial Transactions Carried Out Through Digital Channels

2,199,379,192

Ziraat Bank serves its customers with a rich and diverse digital product portfolio and carries the customer experience to the next level through the effective use of digital channels.

Aiming to provide the best experience, starting from customer acquisition to meeting all customer requirements, the Bank has placed the digital transformation, which it considers from a broad perspective, as the most important component of its widespread growth strategy.

Ziraat Bank’s total number of active digital customers reached 23.1 million as of year-end 2024. The total number of financial transactions conducted through digital channels during the year amounted to 2,199,379,192.

In Q4 2023, the ratio of non-branch financial transactions to the Bank’s total financial transactions was approximately 95.62%, while the digital channel utilization rate increased to 96.60% in Q4 2024.

According to data from the Banks Association of Türkiye, Ziraat Bank accounted for 20% of the total 114 million active digital customers in the banking sector in 2024. As of year-end 2024, the number of active digital banking customers of Ziraat Bank, the bank with the most active digital banking customers in Türkiye, increased by 5% compared to the same period last year, reaching 23.1 million people.

In 2024, the number of the Bank’s customers who made transactions only through the Internet Branch and Ziraat Mobile and never used the branch increased to 14.6 million people; the number of customers who made transactions only through the Internet, mobile and ATM and never used the branch increased to approximately 16.6 million people.

Financial Technology-Based Investments and Projects Supporting Digital Banking

Establishment of Ziraat Dinamik Banka

The BRSA provided the permit for the establishment of Ziraat Dinamik Banka A.Ş., being set up to provide digital branchless services in line with the Bank’s vision and strategies for the future. Ziraat Dinamik Banka is the first digital bank in Türkiye, established under the ownership of a financial group, having received BRSA approval on 31.10.2024. Ziraat Dinamik Banka is expected to complete its integration endeavors with external institutions and start accepting customers in 2025.

Establishment of ZiraatPay

In order to expand its competencies in the field of payment systems and financial technology development agility, and to reach a wider customer base, Ziraat Bank established its new subsidiary, Ziraat Finansal Teknolojiler Ödeme Hizmetleri ve Elektronik Para A.Ş. (ZiraatPay), which received the go-ahead for its establishment from the CBRT. ZiraatPay has received approval to operate as a payment services and electronic money institution with the decision of the CBRT dated 30.01.2024 and plans to make its national launch in 2025.

Ziraat Super Branch

With the Ziraat Super Branch service model, the Bank provides retail customers with straightforward, secure, rapid, and easily accessible banking services via digital channels, supported by centrally located portfolio managers. Since its launch in 2023, the Ziraat Super Branch has successfully reached 1,200,000 customers by the end of 2024.

Ziraat Super Branch customers are offered advantages in terms of interest rates, fees, and limits for many banking products such as deposits, loans, money transfers, investments, and credit cards. The “Super Branch Request/Document Submission Screen” has been redesigned to enable Ziraat Super Branch customers to submit their requests quickly and effectively. This innovation was recognized with the Bronze award in the “Innovative Customer Interaction and Experience” category at the PSM Awards 2024.

Ziraat Super Platform

In 2024, we collaborated with 17 companies to boost the Ziraat Super Platform, a digital ecosystem designed to provide exclusive benefits to Ziraat Super Branch customers through partnerships with companies from various sectors in non-banking products and services.

ZBorsa

The ZBorsa application, which was launched in 2023 by integrating Ziraat Investment functions into Ziraat Mobile banking application, enabled customers to monitor their investment transactions via mobile application and easily manage their investments.

Open Banking

With the Open Banking application launched in 2023, Ziraat Bank offers customers the ability to view their account movements and balances in other banks and institutions from Ziraat Mobile and Internet Branch and to transfer money through Ziraat Bank digital channels. Individual and corporate customers are provided with quicker and more efficient access to banking services.

Virtual Assistant

Ziraat Bank customers can initiate text-based conversations with customer representatives via the Live Chat feature of the Virtual Assistant available on the Internet Branch and Ziraat Mobile.

Z-Transformation Project

As part of its strategy to establish a digital financial ecosystem, Ziraat Bank continues to add new services to its Z-Transformation Packages, which aim to contribute to the digital transformation of SME customers. In this context, as of 2024, legal entity customers and sole proprietorships have been granted access to the E-Transformation Platform (pre-accounting, e-invoice, e-archive, e-dispatch note, e-ledger, etc.), E-Commerce and E-Export Solutions, Office Applications, Vehicle Management, Ziraat Bank Payment Products and Financial Agenda, Bankkart Member Business Platform, and Open Banking Transactions from the Z-Transformation menu.

Digital Slip

In order to support sustainable banking, digital slips were produced instead of physical slips for transactions carried out using Ziraat Bank cards.

Products and Services Migrated to Digital Channels

The Bank’s agricultural loan customers are now able to make loan allocations up to TL 100,000 on their own through Internet/Mobile Banking without visiting a branch.

To reduce operational workload at branches and in-branch customer costs related to TOKİ (Housing Development Administration) Land Loan Repayment transactions, TOKİ Land Loan Installment Payment transactions have been made available on Internet/Mobile Banking platforms, enabling customers to complete their payments digitally.

Development Activities in Digital Channels

Ziraat Bank carries out development and improvement activities to increase the diversity of products and services in digital channels offering a wide range of transactions, and increases customer satisfaction and loyalty by enriching the digital customer experience with new functions. In this context, key improvements implemented in 2024 are outlined below.

Remote customer acquisition through phones with no NFC feature

A new customer remote acquisition process has been introduced for individuals wishing to become customers of Ziraat Bank via Ziraat Mobile without the need to visit a branch, specifically for those whose phones do not support NFC functionality. Under this new process, individuals who are unable to verify their Turkish ID Card due to the absence of NFC functionality on their device can still establish their customer status by transferring funds from their own personal bank account.

Monitoring of branch and ATM densities through Ziraat Mobile and the corporate website

Customers were allowed to monitor the average waiting time at the branches and ATMs in the nearest location for transactions to be made at Ziraat Bank branches and ATMs via Ziraat Mobile and the website.

Easy access to Bank shopping credit facilities from e-commerce sites

Ziraat Bank completed its work within the scope of its business partnerships with e-commerce sites and provided access to the Bank’s shopping loans for customers who need financing during their shopping on the e-commerce platform.

Reducing the number of clicks on digital loan application and allocation

To reduce the number of clicks during the contract steps on the Digital Loan Application and Digital Loan Allocation screens, the process was simplified and the customer experience enhanced by introducing a button allowing agreements to be viewed in a single display.

Expanding the QR Share feature on digital channels

The scope of the QR Share feature on Ziraat Mobile, which was previously made available to the Bank’s retail customers, was expanded and made available to corporate, corporate monitoring, and retail Internet Banking customers through Internet Banking and Ziraat Mobile channels.

Adding FAST Operations menu to Ziraat Mobile login screen

FAST Transactions menu has been added to Ziraat Mobile login screen. The menu enables customers to execute money transfers, perform TR QR code transactions, make payment requests, and carry out secure payment transactions, while also facilitating easy address management. Customers can also perform their trading transactions securely and easily with the Secure Payment Transaction available in the FAST Transactions menu.

Launching the Secure Payment System for Used Car Sales to serve customers

The Secure Payment System for Used Vehicle Sales, which works in integration with the IT System of the Notaries Union of Türkiye for the simultaneous and secure exchange of the ownership of the vehicle in question and the sale price in the purchase and sale of used motor vehicles, was made available to customers through Ziraat Bank branches, Ziraat Mobile, and Internet Banking channels.

Ziraat Mobile and TOGG system integration

Ziraat Mobile and TOGG system integration was completed by creating an application in “Application Marketing,” which TOGG smart device has, and an uninterrupted service experience was provided to TOGG customers. With the cooperation of Ziraat Bank and TOGG, T10X users can make money transfers, HGS and MTV payments easily from the screens of their smart devices.

Bank products and services on comparison platforms

endeavors have been made to streamline the remote customer acquisition process and facilitate product sales through comparison platforms providing information on banking products and services.

Products and Services Contributing to Sustainable Development Goals

|

Reducing branch visits and carbon footprint by adding new menus to digital channels |

SDG8 |

|

Reducing the carbon footprint by commissioning an alternative remote customer acquisition process for citizens who cannot benefit from Ziraat Mobil NFC feature |

SDG13 |

|

Producing Digital Slip instead of physical slip for transactions made with Ziraat Bank cards |

SDG13 |

|

Z-Transformation Platform contributing to the digital transformation of SMEs |

SDG8 |

|

Extending loans to agricultural loan customers through Mobile and Internet Banking channels |

SDG12 |

|

Allowing TOKİ (Housing Development Administration) Land Loan Repayment Transactions to be made through Mobile and Internet Banking channels |

SDG8 SDG11 SDG9 |

Credit Cards

13.4 Million

Debit Cards

44.5 Million

2025 and Beyond

In order to ensure that Türkiye’s most widely used mobile banking application offers far more than conventional mobile banking services, ongoing renewal endeavors focused on personalization and rapid transaction processing through Ziraat Mobile and the Internet Branch are underway and will be launched in the first quarter of 2025.

The Investment and Stock Exchange Transactions menu in the Ziraat Mobile application is planned to allow users to monitor all investment products collectively or individually from a single interface. With user-friendly monitoring screens, customers can be directed to transaction screens quickly while tracking their investments.

Design and development endeavors are underway to make the Bankkart Mobile application a leader among other card applications in the sector, and they are planned to be commissioned in 2025.

Card Systems

As of the end of 2024, there were a total of 13.44 million Ziraat Bank credit cards in circulation, with a 10.41% share in terms of the number of credit cards and a 12.73% market share in terms of monthly turnover. The Bank is expected to maintain its leadership in this area in the medium and long term. Having reached 44.45 million debit cards in the same period, the Bank also maintained its leadership in the sector in terms of its market share of monthly shopping turnover, with a 21.93% share.

As of the end of 2024, there were a total of 1.77 million Ziraat Bank member businesses and 806,000 physical terminals. With a total turnover of TL 809 billion in member businesses in the fourth quarter of 2024, the Bank maintains its sector leadership with a 17.14% market share in turnover as of the end of 2024.

In the field of card payment systems, Ziraat Bank introduced a number of products and services in 2024 which were tailored to market conditions and setting the Bank apart in the sector by offering a wide array of new features.

Use of CGF (Credit Guarantee Fund) Secured Loans through Credit Cards

The Bank established the infrastructure for the use of Credit Guarantee Fund-guaranteed loans through credit cards as well as debit cards in certain sectors, thus contributing to the use of loans in accordance with their intended purpose, the promotion of a cashless society and tackling the informal economy.

Bankkart Prestij/Prestij Plus

Bankkart Prestij and Prestij Plus, special card products creating higher value propositions for the Bank’s upper segment customers, were introduced.

Bankkart Pensioner

Work is underway on the Bankkart Pensioner card product, which is specially designed to meet the requirements of the Bank’s retired customers.

TROY HCE Project

TROY HCE mobile contactless payment solutions have been developed to support the Turkish national scheme.

Digital Slip

In order to support sustainable banking, digital slips were produced instead of physical slips for transactions carried out using Ziraat Bank cards.

Bankkart Mobile POS

The Bankkart Mobile POS offers a fast and practical solution to member businesses by turning Android-based devices into payment terminals.

Payment by Link

Thanks to the link payment feature, member businesses can collect their payments easily and quickly by sending the payment link to their customers.

Efficiency-Oriented Operational Processes

Within the scope of its operational activities, Ziraat Bank has successfully implemented a wide range of systemic improvements in order to offer its customers the best experience in all branches and digital channels.

Thanks to the automation endeavors carried out in line with the goals of streamlined back office operations by simplifying screens and processes and increasing the efficiency of operational processes through the addition of new and user-friendly functions to business processes, around 273 million transactions were carried out through the Operations Center (OPIM) in the 2024 operating period.

The main improvement and development activities carried out by the OPİM in 2024 are listed below:

The reconciliation information requests, most of which were prepared manually by the branches, were fulfilled with a single report and the report titled “Audit Firms Reconciliation Information” was made available to all corporate and commercial branches and regional offices of the Bank via Raportal.

The “Request Payment” function, operated by the Interbank Card Center (BKM) and providing a practical solution for money transfers, was made available in the Internet Banking and Ziraat Mobile Money Transfers menu.

With the improvement made in the collection of loan enforcement proceedings;

It has been ensured that the collection for loan enforcement proceedings is performed automatically in case there are 100-102-106 coded foreclosure blocks (for which a Bank pledge receivable has been reported) on the customer account. It has been ensured that the foreclosure block(s) are defined in the same way in case of a balance remaining in the account following the collection for loan enforcement proceedings. It has been ensured that foreclosure block(s) are automatically removed if no balance is available in the account.

As part of the endeavors to develop the Innovation in Operations (OPİ) functions, the integration of the following transaction types into OPİ was completed; Approval of Bulk Transfer/EFT Files Uploaded from SFTP from the OPİ, Bulk Foreign Currency Transfer, Bulk Advance Import Transfer, Bulk Import Transfer Against Goods.

Payments made through the Central Payment method were allowed from the Bank’s ATMs.

The Secure Payment System was integrated with the FAST system operated by the CBRT, and the upper limit of the FAST transaction amount specific to the Secure Payment Transaction was set at TL 2 million, enabling piecemeal payments.

ATM cash disputes were allowed to be submitted through all channels.

With the improvement made in cash retention disputes in relation to TAM ATMs;- When responding through the Branch/Money Group Centers Approval Transactions Screen, a panel integrated with the SKITMTKK-Cash Difference Reconciliation screen is opened, and the records of the TAM ATM where the retention is experienced are listed.When the transaction is approved by selecting the difference(s) for the disputed transaction, the cash difference is closed automatically.As a result of the favorable or partial favorable closure of the objection by the user of Bileşim A.Ş., the disputed amount is automatically returned to the customer account.

An arrangement has been made for domestic subsidiaries to request authorization by sending a job request via the Anahtar system. User and authorization management of Ziraat Katılım users’ Anahtar accounts has been automated.

Lien transfer transactions have been allowed to be sent via FAST.

In the event of a customer’s death, based on the death information received from the Identity Sharing System, an automated batch process running daily has been implemented to remove the restriction block from the customer’s account.

Deposit transfer letters for accounts under lien, received from the RA, are now rendered legible by a robotic system, with the entry process subsequently carried out and automatically approved by the system.

Corporate Credit Card collections can now be made through the OPIM.

Bulk EFT-Transfer from more than one debtor account has been enabled.

While making a request from the Work Request Entry screen in Card-to-Card Transfer and Credit Card Receivable Balance Refund transactions received by the OPIM BB workflow system, the positive balance on the relevant credit cards can be monitored and the credit balance refund transactions can be completed automatically by transferring it to another card.

Instant Bulk Money Transfer Structure has been integrated into the OPI, enabling instant bulk money transfers.

Endeavors on the process of opening accounts and issuing cards to the paymasters of the institutions affiliated to the General Directorate of Accounting was concluded.

Deposit Research response letters are now sent via the Registered Electronic Mail (REM).

Customers who experienced cash retention during transactions at Ziraat Bank and other banks’ TAM ATMs have been allowed to file a cash dispute directly through the ATM where the transaction took place.

Corporate customers have been allowed to access the Request Payment system via Internet Banking and/or by downloading the current version of Ziraat Mobile, and to send payment requests and approve incoming requests within their existing authorizations.

The “Scanning Checks with Artificial Intelligence Technology” project, which was implemented as part of endeavors to continuously update business processes in line with current technological developments and innovative solutions, increase efficiency in operational processes, and improve customer experience, was completed.

In the Reading Checks with Artificial Intelligence Technology project, which was developed using the Deep Learning method and included algorithms continuously training themselves with new data, with the automatic transfer of all fields on the check, including handwritten fields, to the system;Work flows with high data accuracy are established.The data on the check can be processed faster.Efficiency is increased by minimizing manual processes.

Expropriation Transactions, which were in the pilot implementation stage, have started to be carried out by the OPİM BB.

The Job Request Initiation via E-Mail project, which was developed to respond quickly to customer requests and to increase the quality of service offered to customers by ensuring effective portfolio management, has been completed. Thanks to the improvement, portfolio representatives can send an email during customer visits to automatically file a job request. It has been allowed to take the necessary actions by following the process both through ZFG Mobile and Anahtar.

Data Analytics Projects Providing Added Value

Data Governance Processes Project

The System integration of Data Governance Processes has been achieved. The integration, carried out to comply with legal regulations and establish a data-oriented corporate culture which derives value from data, is capable of reaching data-based decisions and places data at the heart of change.

Data Quality Project

With the Data Quality Project carried out as part of data governance processes, Ziraat Bank ensured that the quality of data in the Bank is measured in line with the determined quality dimensions, data quality is improved, and data is corrected at the source to ensure data-based decision making.

CRM Projects

A customer-oriented service approach was developed through these projects, ensuring that the right suggestions are provided to the right prospective customers via the right channel and at the right time.

Robotic Processes

Ziraat Bank’s customer acquisition processes were supported by robotic process automation, and reporting activities were carried out more rapidly and in a manner that reduced the operational workforce.

Digitalization in Credit Operations

In order to increase the effectiveness of credit risk monitoring and management, the Quarterly Credit Assessment processes were reconsidered and necessary system improvements were made to ensure a more effective monitoring activity. As part of the improvements made in this regard;

The evaluation screen has been made more user-friendly, and the Early Warning Note, “High Risk Customer” definition, Delay Estimation Probability, Default Probability, TCR (Trade Credit Rating), and TII (Trade Indebtedness Index) information have been added and made compatible with current developments.

With these changes, it is aimed to contribute to the effective monitoring and maintenance of credit quality by enabling the existing portfolio to be monitored together.

As a result of the mentioned improvements, the final credit assessment result, which is proposed as positive/negative by the system for all customers in the current structure, has been made to be decided by our Branches for customers in the high-risk category.

It has been made comparable with the positive/negative evaluations of customers in previous evaluation periods, and ease of access to the evaluations of previous periods has also been provided in a similar structure.

In order to ensure effective management of non-performing loans, the existing GAT module has been improved. In this context;

Based on the opinions and evaluations of the relevant business units, the block types that prevent collection have been reduced, and a development has been initiated to subject the overdue receivable to collection over the unrestricted amount to be calculated.

Thus, preliminary work for the transition to a parametric structure to manage the blocks placed on customer accounts has been initiated.

In our Law Office practice, which is in operation for the collection of our receivables with low balances transferred to follow-up accounts through administrative means, the action period, which was 90 days after the transfer, has been reduced to 60 days, saving time and cost.

Improvements in the Early Warning System

The “FX Risk Probability” criterion has been introduced in the early warning system in order to identify and manage customers who, despite having a significant FC risk in their combined records, do not have FC income / have limited FC income according to their current financial data in the Bank’s system and therefore have/increase their vulnerability to possible exchange rate fluctuations.

The “Delay Estimation” criterion has been introduced within the scope of improving the future forecast modeling of the Early Warning System. Based on the behavior of customers who have delayed their loan repayments in the past, the developed model calculates the probability of delay in the future for customers who have not delayed their loan repayments in the past. The model, which will run at the end of each month based on the aforementioned criterion, will predict the customers who are likely to delay their repayments in the next 6 months.

“EMRA License Revocation” criterion has been activated in the Early Warning System (EUS) in order to monitor the Bank’s customers, who carry out their commercial activities with the relevant licenses issued by EMRA, but whose licenses have been canceled, terminated, revoked, or temporarily suspended, and to take the necessary actions.

In the Early Warning System, which is an important tool in the effective monitoring and management of loans, the Default Probability field was added to the Early Warning History (EUSRFRMK) screen in line with current developments, enabling the monitoring of the default probability history of customers.

Close Monitoring/Blocking Actions

The practice of placing a block on the credit limits of customers who are in delay in their corporate loans at other banks has begun.

Corporate loan allocations of customers with a significant increase in their credit risk within the scope of TFRS-9 are linked to the Default Probability value.

The integrated report addresses the economic, environmental, and social performance of Ziraat Bank for the period between 1 January 2024 and 31 December 2024 under a holistic approach. The report includes information regarding the Bank’s banking activities and its domestic and international subsidiaries.

Your views on how we can further improve our report in the future will guide us. Please share your opinions and suggestions via e-mail.